Stocks and bonds both opened lower today. One of the news items weighing on the stock market is retaliation tariffs from China. China announced that they will increase their tariffs on 128 US products, which is now reigniting fears of a trade war and ugly politics in Washington.

Today’s economic news that affects mortgage rates is quiet. However, it will be a busy news week highlighted by the Initial Jobless Claims Report coming out on Thursday morning.

This Week’s Economic News

The ADP Employment Change Report and the BLS Jobs Report will be released Wednesday and Friday respectively. The most recent Jobs Report showed that wage increases rose by 2.6 percent year over year. There are many in the media who are of the opinion that when you compare that to home price appreciation, homes are becoming unaffordable. The latest Case Shiller Report showed that home prices rose by 6.3 percent over the past year. When you look at these two numbers it’s easy to see why some are of that opinion. But it’s also important to remember that the bottom 25 percent of the wage earners are typically not in a position to buy a home. Year over year, their earnings actually decreased by 2.5 percent. That indicates that the rest of the job pool had to go up at a higher rate to come up with a national 2.6 percent increase. They would have had to rise by 4.7 percent. There are still some who say that is not as high as 6.3 percent that we saw in the Case Shiller Report.

We also have to remember that incomes never keep pace with home appreciation and don’t have to because of the relative relationship typically between home and payment and income. It is not uncommon for the income of a household to have a 5 to 1 ratio of their home payment. If a person was looking to purchase a home and their monthly payment (principal and interest) was $1,000 per month, but they decided to wait and home prices rose by 5 percent, their payment would go to $1,050. If their income was $5,000, it would only have to rise by 1 percent to match the $50 increase. So a 4.7 percent rise in incomes for those who are buying homes can more than support a 6.3 percent appreciation rate.

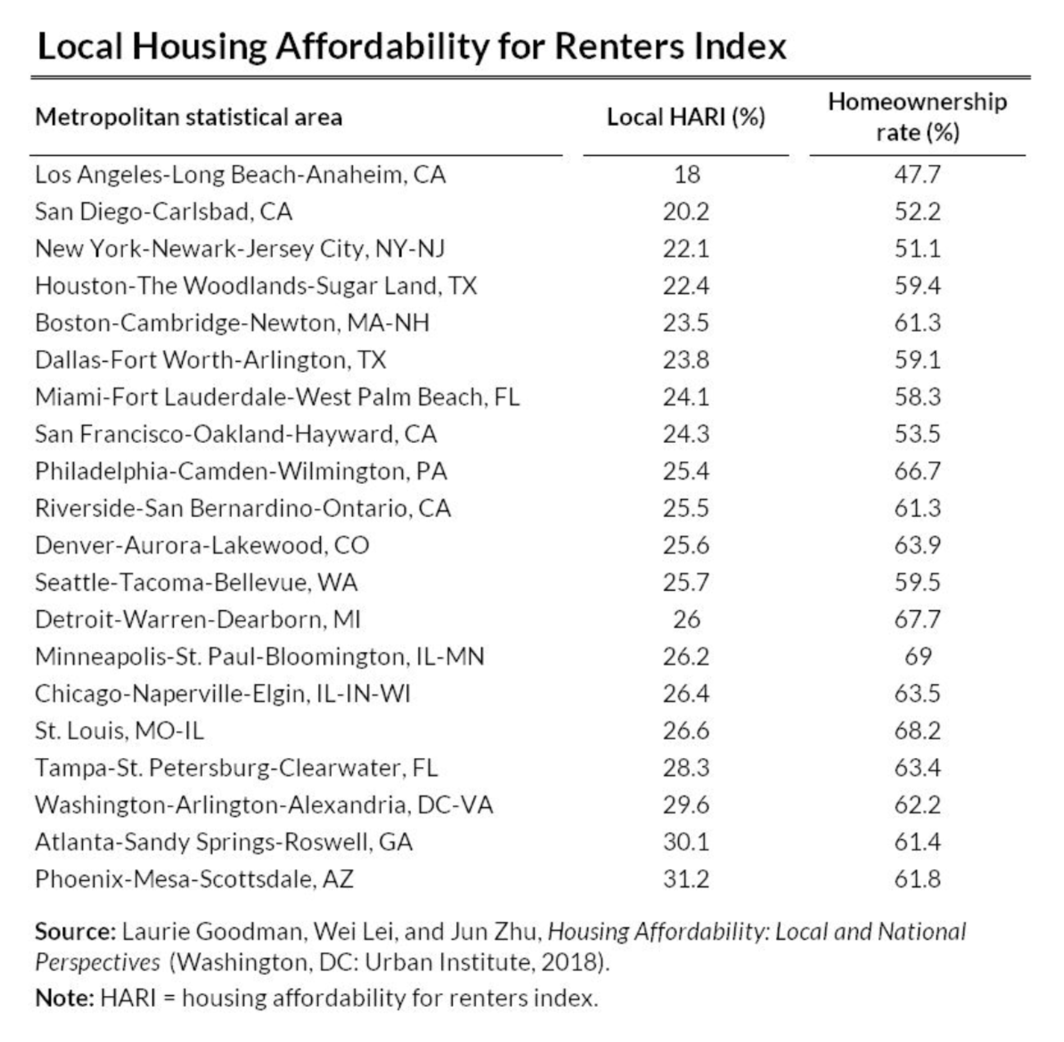

Buy vs Rent?

The Urban Institute wrote a very interesting article on their new HARI (Housing Affordability for Renters) Index, which shows that certain cities are more affordable for local renters than other measures indicated and about 1 in 4 renters have incomes that put home ownership within reach. The chart below shows that homeownership in the 20 most populous MSAs (Metropolitan Statistical Area) as well as the local HARI, which shows what percentage of those renters can afford to buy a home.

Mortgage Rate Forecast

The FNMA 30-year 4.0% coupon bond ($102.609, +25.0 bp) traded within a narrower 45.3 basis point range between a weekly intraday low of $102.188 on Monday and a weekly intraday high of $102.641 on Wednesday before closing the week at $102.609 on Thursday.

Mortgage bond prices were able to rise above their 25-day moving average resistance level ($102.34) that now reverts to nearest support, and continued higher toward their 50-day moving average ($102.69) where the next level of technical resistance is located.

The chart below shows the bond is approaching the “overbought” level as it approaches the 50-day moving average, so while there is still room for price improvement, the bond may have a tough time breaking through this level. If the bond can manage to move above the 50-day moving average, mortgage rates should improve slightly. However, if the bond is turned away from this level, mortgage rates would hold steady near current levels.

Jim’s Rate Lock Recommendation

LOCK if closing in 7 days

LOCK if closing in 15 days

LOCK if closing in 30 days

FLOAT if closing in 45 days

FLOAT if closing in 60 days